This post is about my friend Patrick, who recently found herself on the wrong side of whatever causes Amex to deem someone unworthy of a sign-up bonus. (Yes, Patrick is a lady, and she’s aware she has a weird name for a lady. Her full name is Patrick Pibb, which is hilarious and sounds like a character from a lost Charles Dickens novel.)

Ever since I read about Amex’s new policy (on Doctor of Credit, of course), I’ve been nervous about it. Amex is by far the most lucrative of the three issuers for churners, even after they instituted a once-per-lifetime policy on sign-up bonuses. They just have so many damn cards, even if you only get the bonus one time on each card, that will still amount to millions of points. I’ve been churning pretty aggressively for years, and there are still Amex cards I’ve never opened.

I suppose it was inevitable that Amex would crack down further, given how strongly their competitors have been pushing back on churning… first there was Chase’s 5/24 rule, and then Citi’s policy of restricting bonuses to one per card family (something Chase followed pretty quickly with the Sapphire cards). Given the aforementioned ease of racking up Amex bonuses, it was only a matter of time before Amex did something about it. What they’ve done, however, is a horrible abomination. Well maybe not quite, but it sucks pretty bad.

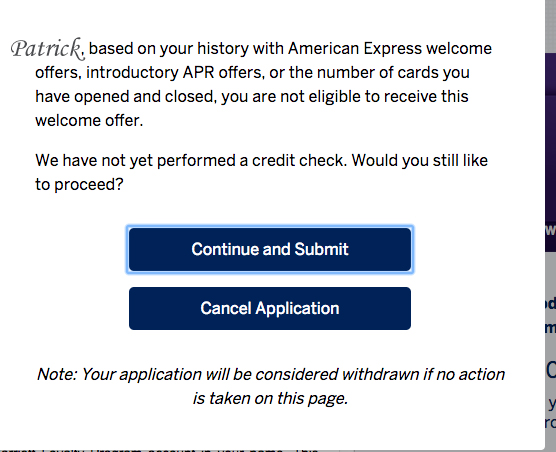

Yes, you saw it here first thirteenth. When you apply for a card, you may now get a pop-up informing you that you aren’t eligible to receive the sign-up bonus. If you hit “continue and submit,” your application will process as normal, and if you hit “cancel application,” the dog from Duck Hunt will pop up and laugh at you.

There’s both good and bad here… the good is that they’ll tell you for sure before they run a credit check, and you can still get the card anyway. This is great for someone who wants a Delta card for the free checked bag or companion fare… since a United flyer in the same position with Chase wouldn’t be able to get the card at all. Ditto Hilton vs. Marriott. The bad news is that it’s now all-or-nothing. Unlike Chase, who gives you the option of waiting out the 5/24 clock, or Citi, with whom you can still earn points from bonuses albeit more slowly, Amex now locks you out of the most lucrative bonus game full stop once you get on their bad side.

Plus, say what you want about 5/24, but at least it’s a published, objective rule. I’ve written in the past about how annoying it is to get denied for a card for “too many recent inquiries” without any indication whatsoever of what constitutes “too many.” Amex is definitely going the ambiguous route here, basically saying that there’s something off about you, but they can’t put their finger on it.

I’m sure as more data points emerge, some of the fog around Amex’s new policy will clear. (I assume the churning subreddit is on the case, asking users to fill out a Google form that asks your age, income, number of cards, number of bonuses, date of any card closures, number of sexual partners, brand of wallet, number of times in Emirates first class, name of nearest bank branch, and other critical info.) For now, though, it’s maddeningly difficult to determine what about someone’s history with Amex makes them ineligible for a sign-up bonus.

In Patrick’s case, she has seen the warning twice. The first time was on an application for the Business Rewards Gold card, and I told her to wait a little while and then try to apply for the new SPG personal card. My feeling was that Amex might be stricter with Membership Rewards cards versus co-brand cards, or that it had something to do with business versus personal cards. Neither of these hunches were true, and she got the same message on her SPG application a couple weeks later.

What’s really strange, though, is that — at least for now — I’m still able to get Amex bonuses. Or at least I was when I applied for the SPG Luxury card the day it came out. If you look at my history versus Patrick’s, I look way more like a churner. I’ve opened nearly 20 Amex cards in the past four years, and I have closed plenty of them as well. In contrast, Patrick has opened four Amex cards since the beginning of 2016 and only closed one of them. Unless Amex was so excited to have people sign up for the SPG Luxury card that they didn’t apply the same restriction that they’re clearly applying to both Amex-branded and co-branded cards, something doesn’t make sense here. (That’s certainly possible, by the way, given that Amex had so many sign-ups for the Luxury card that they ran out of cards.)

I have one other theory… After looking at Patrick’s card history, I asked her one potentially very important question: “How much have you paid Amex in annual fees since you opened your first card with them?” I already knew the answer based on Patrick’s general aversion to paying annual fees: zero dollars and zero cents. While I have certainly opened and closed some cards cards without paying the annual fee, I have also paid the fee on multiple platinum cards, my green card, the Everyday Preferred, a Delta Platinum, and a bunch of others.

Given that bonus eligibility is an instant calculation, there’s obviously some algorithm in play that evaluates how valuable of a customer you are for Amex. Despite my aggressiveness opening Amex cards over the years, for whatever reason, the algorithm thinks I’m more valuable to Amex than Patrick, and the thousands of dollars in annual fees that I have paid may play a part in that. Of course I’m just speculating here, and as noted above, most of my theories around this whole development have turned out to be wrong. (Just more evidence of how cruel it is for Amex to keep everyone guessing from now on.)

Who has had recent success/failure with Amex lately? I don’t want to get into Reddit-level data collection or anything, but I’m curious if Patrick is an outlier, or if I’m the one who got lucky sneaking past the gatekeeper to get my bonus on the SPG Luxury card.

Support your windbag!

This site is ad-free, because I think ads are ugly. That's why I rely on readers for support! If only one person per year gives me $5, then I'll have $5 more per year. Everyone wins!

$5.00

Man, I’d like to know what is up with AMEX too! Just successfully appd for the Blue Biz Plus card, through the online thing for the 10k MR, yet nobody at Amex can say I am getting the bonus once I hot the spend. NO pop-up though when I applied and I think I am good. Small bonus but hey! 10k is 10k!

LikeLike

I recently applied incognito for Gold Rewards card aiming to get 50K sign up bonus but got the same dreadful pop up. Being “slightly tipsy” I called and grilled Amex customer support until some guy told me I haven’t put enough spending on my cards (I have 2 SPG, Delta Gold and Everyday). So spending might be a factor too here.

LikeLiked by 1 person

Thanks for posting this. Patrick Pibb barely spent any money on her Amex cards either.

LikeLike

Can’t say I’ve had the chance/need yet to test the new waters with Amex, but at least I am not dreading it: They seem to have fashioned a no harm / no foul way of saying, “No more for you. At least not right now.”

Whereas some of these reports I have been reading about Chase shutdowns, even for those under 5/24 — and especially the apparent cross-spouse concatenation of these events — has been giving me the willies. One simply doesn’t know what one might do (be doing) to push Chase over the edge (or, better metaphor: for Chase to push you / me over the edge). If I weren’t so addicted to Hyatt, hence UR points and the new Chase Hyatt card, I wouldn’t care so much. But I am, so I do care.

LikeLike

I got the bonus denial today for the refurbished Amex Gold, to my disappointment. I have only opened 6 Amex cards since 2011, and 3 of those are still open. I’ve never had any Amex Gold card. I have paid Annual Fees at least 4 times. Several years ago I had a BCP that I used regularly, and before that I put a fair amount of spend on a Delta card that I no longer have. However, I have put very little spend on my Amex cards in the last 3 years. I use the Hilton card when I stay at Hilton, Delta card when I fly Delta and the EDP for the occasional Amex offer. The early Reddit data is pointing towards lack of spend as the problem. I wonder how much you have to spend to make them happy? Maybe I should start MS-ing again.

LikeLike

More importantly, There are chicks named Patrick?

LikeLike

Well, one chick.

LikeLike