Quick Windbag Miles update: I have a podcast now! It’s only accessible if you’re a Patreon subscriber, though, so if you want to listen to my dulcet tones, consider supporting the blog with your money in addition to your eyeballs. As of this writing, I have eight subscribers, which means that, yes, I make a podcast that only eight people are able to hear. Okay, now on to your [ir]regularly scheduled blog post…

Earlier this month, I wrote about Morgan Stanley’s suite of Amex cards, which includes a basic no-fee card and a co-branded version of the Amex Platinum. This post is a continuation of some of the topics I talked about in that post, with a focus on the “Invest with Rewards” benefit, which allows you to cash out Membership Rewards points into a brokerage account at $.01 each.

The previous post goes into more detail about why this may or may not be a good deal. After all, a penny each isn’t a great value for Membership Rewards points, especially when the Charles Schwab Amex Platinum cashes out at a ratio of 1 point : 1.25 cents. However, depending on your individual needs and how many points you realistically plan to redeem this way, it could make sense to use Invest with Rewards. Here are a couple ways it could make sense:

-

You’re averse to annual fees, so you don’t want either the Charles Schwab or Morgan Stanley Amex Platinum cards. If you want to backstop your Membership Rewards balance with a cash-out option, the no-fee Morgan Stanley card is your only opportunity (since the no-fee Schwab card earns cash back, not points).

-

It’s important for your spouse to have an Amex Platinum card too, so the free authorized user on the Morgan Stanley card saves you $175 per year. If you plan to redeem less than 70,000 points per year, you’re actually better off with Morgan Stanley’s inferior cash conversion after you factor in the authorized user fee you’d need to pay on the Schwab card.

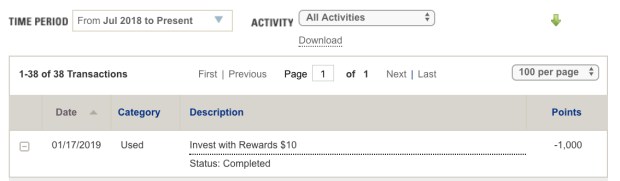

Unlike Schwab, however, cashing out points with a Morgan Stanley card is a little more convoluted. Instead of doing everything through the Membership Rewards portal, you have to go to your Morgan Stanley account and then back through Amex to get it done. It took me forever to find it in my MS dashboard, but I’ll save you the trouble: it’s under the “Services” drop-down menu.

Clicking that link will take you to an Amex webpage that’s separate from your online account.

Instead of logging in, you enter in a bunch of information about your card in order to verify that you’re eligible. Then you reach a somewhat cumbersome menu to select how many points you want to use, along with a dropdown menu to select the brokerage account into which you want to transfer the funds. (This is the same mechanism that the Schwab card uses, which leads me to believe that there’s no reason why Morgan Stanley has to make it more difficult.)

I was really happy to see my Access Investing account listed here, since it confirms that the whole Access end-around to get the Morgan Stanley card was never a backdoor in the first place… turns out the person I spoke to on the phone who told me that Access accounts didn’t qualify for Morgan Stanley Amex cards was wrong. (And we just won’t talk about that whole “open an Access account but never fund it” trick.)

After not one but two screens asking me if I was absolutely SURE I wanted to do this, I got a confirmation and the points were immediately deducted from my Amex account. The confirmation said that the funds would take 4-6 business days to show up in my Access account, but when I logged out and back in, the money was already there.

And that’s it… harder than Schwab, but not that bad. It’s great to know that this feature still works with Access accounts, and that the error I kept running into the last time I tried to test this was just a random glitch.

Finally, I was thinking about how these points-to-investments features really fuck with the valuation of points in a hilarious way. There’s been a lot of discussion about the value of points lately, and I swear every time I hear people debating what points are worth I care about the subject even less. But, for those people that want to get really scientific about it, I present this scenario to you, which I call “The Membership Rewards Ouroboros of Tautological Value.”

-

You cash out 27,500 points into $275.

-

The market doubles, and your $275 investment is now worth $550.

-

You spend $550 on the annual fee for a version of the Amex Platinum card you haven’t had before, effectively buying 60,000 points for $550.

-

But you paid 27,500 points to get that $550!

-

Which means that Amex points are worth more than twice what they’re worth.

-

Unless you do it again and the market drops by 2/3, in which case Amex points are worth…. [head exploding gif].

-

Okay Frequent Miler, have at it!

-

(J/K please don’t stop linking to me because like 70% of my traffic comes from you.)

I’m still curious, though… would anyone ever actually cash out a meaningful amount of Membership Rewards points at a penny each, besides some dumb blogger who decides to waste 1000 points “for the content”???

Oh hey don’t forget that Patreon page!

Okay, I’ll admit it. I might as well have the capacity to cash them out at a penny a point, since all I ever do is use them to buy American Airlines tickets. This was justifiable when I got the Amex Business Platinum and it was rebating 50% of points, then mostly justifiable when the rebate was 35%. Now, without the card (no retention offer, you just see if I won’t cut off my nose to spite my face!), at best I can get 1.05 if you count the standard 5% Amex Insiders fares.

Seriously — not argumentatively: What should I be doing with these supposedly hypervaluable points? I don’t fly to Asia. I do fly from PHL. There are lots of wonderful nonstops from PHL to Europe, and I do like to fly in J. But I don’t know how to connect MR points to AA. (And I would much rather fly in MCE or PE nonstop than have to make my way to EWR or — shudders — JFK.)

The other rationale for this pointless behavior, which I can’t even attribute to blogging, is that using MR points for AA tickets is essentially like using them as American (USA) pennies. These non-award tickets do help me make it to at least Platinum each year, and that lets me get exit aisle MCE seats for my dreary but compulsive stateside travel.

Why do I collect MR points at all? I was going to stop, but then they hand out referral offers… I mean, jeez, if you don’t recomment your spouse for a Blue for Business, then you must be the kind of person who doesn’t stop to pick up $100 bills blowing on the lawn.

LikeLike

So if you have both this and the Schwab plat…. can’t you just redeem it into the Schwab checking account at 1.25 cents per point instead of MS’s????

LikeLike

You could, but I was assuming that most people wouldn’t have both cards open at the same time.

LikeLike