Wow, I’m actually writing a blog post! It was bound to happen sooner or later, since all kinds of wacky crap has been happening this year, and I’ve felt the percolations of motivation tickle my brain more and more frequently lately. What finally put me over the edge? I got an offer on my lowly Barclays Arrival card (not the Arrival+, mind you) — AKA the card I recently used for a $5 Amazon reload because Barclays told me they were going to close it if I didn’t start using it again — and it’s such a really, really, ridiculously good-looking offer that I just had to write about it. (As a quick aside, I do appreciate the advance warning before they closed the card for inactivity and wish more banks would do this instead of just closing the card and letting you know after the fact.)

I started over on Twitter (that’s right, I’m still tweeting with abandon), with this observation:

I might as well get to the point and tell you about the offer, although I’m not going to lie… it did occur to me to write this entire post and never mention it, just to be a stinker.

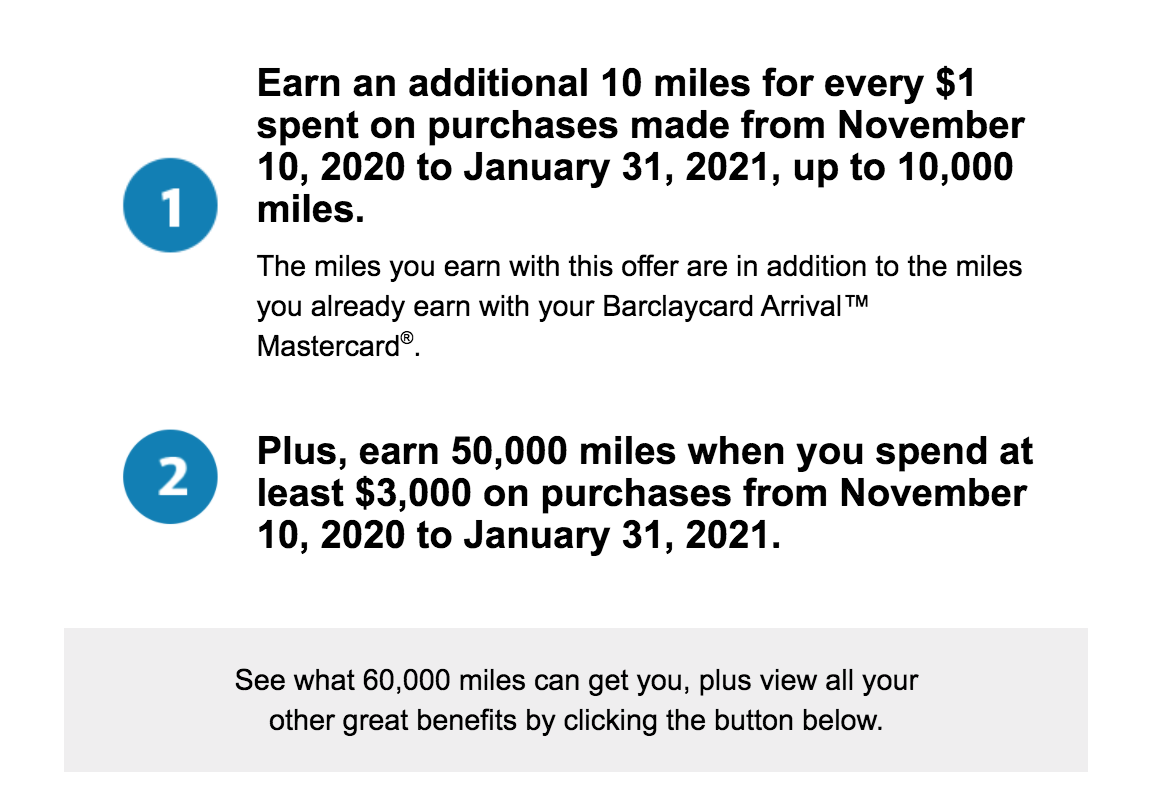

Yes, you read that right. 11x points per dollar up to $1000 in spending, with no category restrictions. Then 50k for spending $3000 over the next couple months — again with no category restrictions. Did I get this offer because I cockteased Barclays with my $5 Amazon reload and they are just desperately trying to weasel their way back into my wallet? Do they really need me to spend $3000 so badly that they’re willing to give me $600 worth of points before I shoebox this shitty card until they threaten to cancel it again?

(Another digression: The incongruity between the strength of this offer and my value to Barclays as a customer reminded of the post I wrote last year in response to an article that suggested that it’s unethical to open a card just to get the sign-up bonus without actually intending to use the card. I’ve only paid an annual fee to them one time (on an American Airlines card that I then used to game the shit out of their program that essentially let you buy AAdvantage miles for $.01 each), and I’ve never carried a balance. I got the Arrival+ in order to get a 60,000 point sign-up bonus, spent the minimum on it, and then put it away until it was time to downgrade it to the no-fee version. If they want to give me $600 to entice me to do more business with them despite my history with them, I’m not gonna argue.)

The reason I was motivated to write this post is that Barclays’ overall credit card strategy makes so little sense to me, I can’t help but marvel at it. (Whenever I write posts like this, some killjoy always shows up in the comments to chastise me for thinking I know better than a giant financial services firm, and my response is always the same: my irreverance is always going to be less cringey than your need to defend giant financial services firms in the comments of obscure blogs with less than 100 monthly visitors.) Anyway, when I first got into the credit card game, the Arrival+ was one of the main “it” cards. The Sapphire Preferred and the Arrival+ were the two cards bloggers recommended you start with — transferrable points from Chase and cash equivalent points with a great everyday earning rate from Barclays. I even wrote a very embarrassing and overwrought explanation of my methodology for benchmarking the value of transferrable points against the 2.2 (at the time) points you were able to earn per dollar with the Arrival+, so consumed was I with deciding what would be the best option for me.

It ended up taking me a while to get around to actually getting the Arrival+, since I was too consumed with transferrable points to care much about having cash equivalent points as well, although that time rolled around eventually. By that time, Barclays had started chipping away at the overall value of the card, reducing the redemption rebate from 10% to 5%, upping the minimum points needed for redemptions, and other stuff like that. But, they made up for it by increasing the bonus from 40 to 50 and eventually 60k, which I certainly appreciated.

However, despite having an undoubtedly successful card on their hands — a perennial favorite among the Boardingarea set — it honestly seems like Barclays then fired their head of consumer credit cards and hired someone away from Synchrony or one of the other semi-subprime retail co-brand card factories. Attention moved away from the Arrival as they promoted co-brands from companies ranging from the NFL to Lufthansa. Then they made waves with an absolutely laughable high-end Arrival card that had no sign up bonus and was designed to encourage long-term loyalty. They somehow thought this card could compete with the Sapphire Reserve, despite it being described as a “wet turd” and a “lead balloon.” (Well, that’s how I described it, at least.) It was funny to see bloggers with Barclays affiliate links twist themselves into knots trying to justify how that card was worth applying for, but it was only around for a matter of months (if memory serves) before they stopped accepting new applications.

That Arrival card (I can’t remember the actual name, but let’s call it the Arrival Minus) came about at a time when churning was becoming increasingly popular, and banks were starting to get some acid reflux thinking about all the points they were giving away. Citi and Chase implemented “once per family” rules across their card families, and Chase doubled the bonus ineligibility period on the Sapphire cards. At the time, I opined that this was always going to be mitigated by higher targeted offers, since consumers had made it clear that big sign up bonuses were the only way to motivate mass enthusiasm around a credit card. (My reasoning was that every attempt to encourage long-term loyalty by setting up tiered sign-up bonuses that require keeping the card for longer than a year was eventually abandoned by the issuer.)

But, Barclays didn’t come back with a retooled Arrival card at all… they just quietly killed the Arrival Minus and that was it. Now when you go to their site, you can see cards from a dozen travel and retail brands, but nothing with their own points currency. The entire Arrival brand is relegated to the trashbin of churning history. It begs the question of exactly why they’re trying to encourage me to engage with the Arrival family to begin with — especially since I can’t get approved for any other cards due to their restrictions on having too many applications. If they’re going to throw bonuses at me, wouldn’t they rather do it via a sign-up bonus on a card where I’d have to pay an annual fee right away, or at least a card that’s a current/continuing product for them rather than a relic of the past?

I suppose I shouldn’t think too hard about it and just accept the offer and move on. After all, it is quite possibly the strongest “continuing spend” offer I’ve ever received on a card, and I’m certainly appreciative of it in these income-depressed COVID times we continue to live in. If Barclays’ internal metrics have identified me as a customer of value, I should just be flattered rather than thinking there must be some malfunction at the corporate level to single me out. (Is this part of my middle-child syndrome that I desperately crave validation while suspecting that anyone who validates me is making some kind of mistake?)

TL;DR: Barclays has a great offer going on Arrival cards, and I don’t know why the hell they’re even bothering. It confused me so much that I wrote the first new post on this blog in over a year. Yay?