One of the pleasures of a new Amex card is setting up all the benefits that must be added manually. For any card that earns airline incidental fee credits, that means manually selecting an airline. I’ve always picked United in the past, since Gift Registry contributions are usually reimbursed… although with United’s Gift Registry page unavailable for the past couple months, I’m considering switching to American and trying my hand with e-gift cards.

However, any time I have tried to select American with my new card in the past few weeks, I have received this error message:

Anyone else dealing with this? The end of the year is rapidly approaching, so I’m hopeful that Amex fixes it soon. I can always try calling, but I’m lazy. That’s why I’m writing this whole blog post rather than taking the same amount of time to call Amex and resolve it.

Hey, if you’re new to this blog, check out my page on credit card info for other articles you may like. And since I don’t run any ads on this site, I depend on readers for support (via Patreon). Thanks!

schwabamex.jpg

I made the switch this year from Amex’s normal Platinum card to the newish Charles Schwab Platinum card, mostly because I wanted to get another sign-up bonus. After Amex revamped the Platinum card and raised the standard bonus from 40k to 60k, the Schwab card followed suit, so when it came time to renew my Platinum card this year, I canceled it and opened the Schwab card instead. It seemed like an even trade, since the Schwab card has all the same benefits – the only downside is that it doesn’t offer referral bonuses… although my wife was the only person who ever used my referral link, so I don’t see that as a great loss.

Otherwise, the Schwab Platinum is identical to the normal one, down to the look and feel of the card, the welcome packet, and the benefits… save for two special enhancements for Schwab customers. The first really only benefits rich people – if you have $250k/$1M with Schwab, you get $50/$200 off your annual fee. If you aren’t sitting on that kind of wealth, you pay full price like anyone else. The second benefit is “Invest with Rewards,” which enables you to convert points to cash in your Schwab investment account at rate of 1 point to 1.25 cents.

When I originally signed up for the Schwab Amex, I didn’t really think much of the points-to-cash conversion, since I generally feel like my points are worth more than 1.25 cents apiece. However, gaming out various travel scenarios and comparing the utility of this feature against other cards, it turns out that it can really work out in your favor.

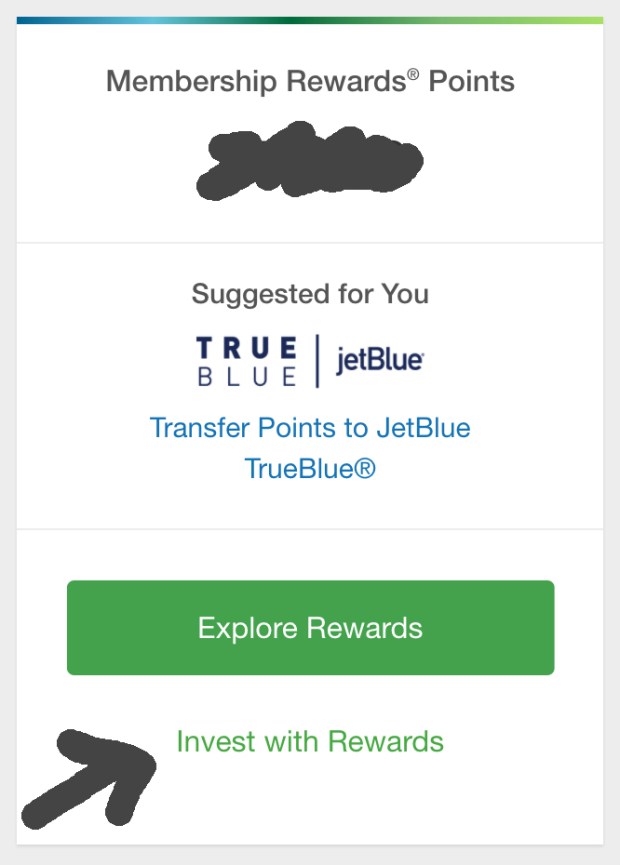

For a quick recap, here’s how it works. When you add the Schwab Platinum to your Amex online account, you’ll see an “Invest with Rewards” option under the normal “Explore Rewards” button:

schwab-1st

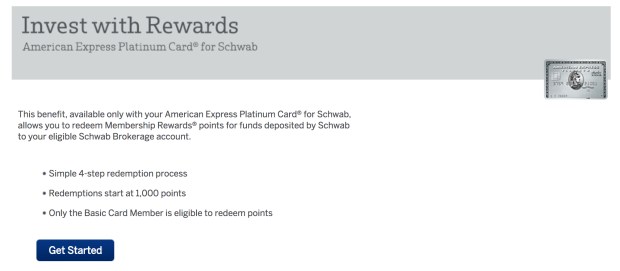

Clicking that will take you to a page with some general info about the program:

schwab-2nd

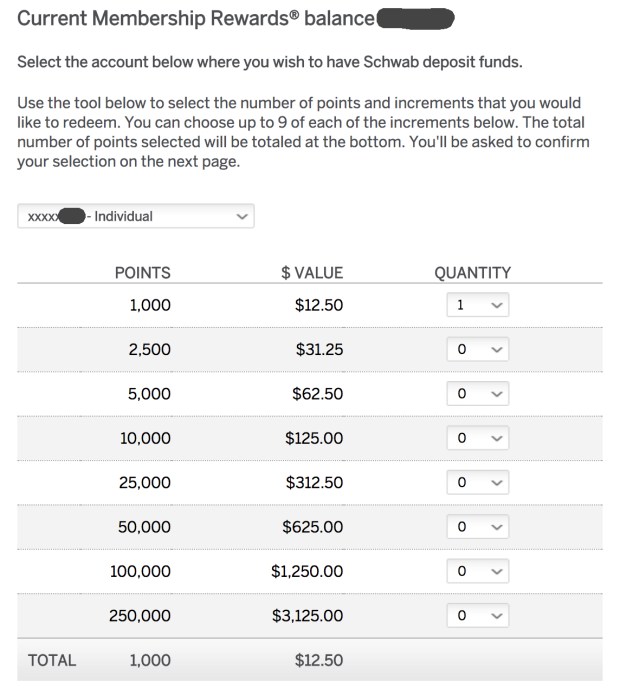

And once you enter some basic card info, you’ll get to select how many points you want to transfer to your Schwab account (in a fairly convoluted manner, I have to say):

schwab.jpg

That’s basically it. I didn’t end up making the transfer, but I went through all the steps before writing this post, mostly to confirm that my entire Membership Rewards balance would be eligible and that Amex wouldn’t limit it to the points I earned with this specific card.

So let’s think about this. If Amex points are worth 1.25 cents in cash, right off the bat they become a lot more useful for strategic travel redemptions. I’m thinking along the lines of using Chase Sapphire points for cheap hotel stays or short-haul flights in situations where you don’t want to pay cash. Flexibility-wise, Amex points are even better, because they’re as good as cash – you aren’t locked into a specific travel portal in order to get the 1.25/1.5-cent redemption value offered by Chase. (Chase points can be redeemed for cash too, but only at a one cent per point value.)

When the Sapphire Reserve came out, a lot of hay was made over the fact that if you combined the Freedom Unlimited and the Sapphire Reserve, you could guarantee yourself at least 2.25% cash back toward travel on every transaction (because the Freedom Unlimited earns 1.5 points per dollar, which works out to 2.25 cents toward travel when transferred to the Sapphire Reserve). However, Amex one-ups this if you add in the new Blue for Business card, which earns 2 points per dollar on all transactions up to $50k per year. That means that the Blue/Schwab combo gets you a minimum of 2.5% cash back period – not just for travel and not just through one specific portal.

2.5% back on everything is a fantastic return. The only other comparable card is the Alliant Visa Signature, which offers 3% cash back the first year and 2.5% each year thereafter. Otherwise, the closest would be the new Bank of America Premium Rewards card, which earns 1.5% or more depending on how much you bank with BofA. However, in order to get the maximum return (2.625%), you’d need to have over $100k on deposit with them. Any less, and you’re better off with Amex.

And, that’s just the return on everyday spending. Leveraging Amex’s entire card portfolio and the attendant bonus categories can really juice your overall cash-back returns.

Airfare and hotels booked through Amex: 6.25%

Groceries: up to 6% if you use a card with an annual fee; 3.75% otherwise

Gas: 3.75%

Everything else: 2.5%

(Quick aside that I’m of course ignoring the Platinum’s high annual fee here. To me, the card justifies its fee in other ways, so I’m not factoring the fee into these calculations. If you simply want cash back, you’re probably best off with a straight 2% cash back no-fee card or the Alliant Visa.)

This is important to me, because I find Amex points to be substantially easier to earn than Chase, just due to the sign-up bonuses available – and especially in the age of 5/24. If you’re maximizing your Freedom and Ink 5x categories with Chase, you’re going to do pretty well, but there are just so damn many Amex cards, I think it’s way easier to build up a six-figure balance in a short period of time. Plus, Amex is more generous with incremental bonuses (such as the 5000-point Amazon Prime renewal offer) and referral bonuses. So, given that Chase points are harder for me to earn, I’d rather save them for aspirational redemptions via unique partners like Korean Air than using them at $0.015 for dink-and-dunk flights or hotel rooms.

Amex has always offered such a vastly inferior value proposition ($0.01 for flights and $0.007 for hotels) that I’ve never considered redeeming Membership Rewards points through their travel portal. However, with this Schwab wrinkle, they become almost as valuable as Sapphire Reserve points, giving me a new option for low-value redemptions that can take some pressure off of my Chase balance. Staying within the world of travel, it’s also really important to consider that low cost carriers don’t always show up in the banks’ booking engines. If you’re looking for a flight around Europe and you want to book through Chase, you’re going to have to redeem your Sapphire Reserve points for flights on legacy carriers that are often 2-3x the cost of what you can find on Norwegian.

It’s an even bigger deal when you look at transatlantic flights. For instance, I’m brainstorming a trip with Justine next year to Venice, and I’m thinking about starting the trip in Rome. You can’t fly direct to Rome from San Francisco, but Norwegian operates direct flights from Oakland. That means that I could transfer 85,000 points to Delta in order to connect via Amsterdam or Paris, with 10 hours in a flat bed and 2 hours in Euro-business glorified economy seats… or I could pay cash to fly direct in Norwegian’s premium cabin, which isn’t as nice as business but is nicer than premium economy on Delta, Air France, or KLM.

Those Norwegian flights go for $700 – $850, so let’s imagine that I need to spend $1700 for two tickets. That means I’d have to transfer 136,000 points to cover the charges. That’s 68,000 points per person, or a substantial discount off of what you’d have to pay in Delta miles. The experiences aren’t totally equivalent, since business class on a normal airline is substantially better than Norwegian. However, considering a direct flight vs having to connect (especially given the shit-tastic quality of intra-Europe business class) does bring the two options closer in line with each other. It also means I have way more flexibility planning the trip and don’t need to worry about finding saver availability.

Consider also that if I pay for the Norwegian flights with my Platinum card, I’ll earn 8500 points, bringing the total per person down to 63,750 points. That’s roughly equivalent to what I’d have to spend if I transferred points to Flying Blue (assuming I do so before Flying Blue self-fucks their program with an iron rod), although in this scenario, I’d also avoid paying $250-$300 per person in fuel surcharges.

The Schwab Platinum card isn’t the only Amex card to offer interesting redemption options for Membership Rewards points, by the way. The Business Platinum does have the compelling benefit of offering a 35% rebate on pay-with-points travel redemptions, but there are some catches. First, of course, you’re locked into Amex’s travel portal. But even if you assume you’d be able to book those Norwegian flights, you’d then have to have 170,000 points in your account in order to purchase the flights, and you’d have to wait for the 59,500 points to be credited back to you. Ultimately you’d pay right around 55,000 points per ticket, which isn’t even that much less than the Schwab option described above.

Low-cost premium cabins like Norwegian’s and the new seats supposedly coming to WOW Air will be increasingly important to me as more and more opportunities for aspirational redemptions dry up. Just look what’s happening with Flying Blue and British Airways Executive Club… Chart-based redemptions aren’t going away immediately, but the process is definitely picking up steam. All along I have said that once chartpocalypse finally comes, I’ll turn my focus to working cash back cards in order to afford the cost difference between economy and premium on low-cost carriers. Now I’m realizing how lucrative the Schwab Amex can be in this scenario.

In the end, I’m not going to forsake transferring points to frequent flyer programs or anything – I’m just happy that I more or less stumbled into a new redemption option for my points that can make a lot of sense in certain cases.

(Finally, in case you aren’t familiar with Schwab, it’s actually really easy to get an account with them. It isn’t like Morgan Stanley or Ameriprise that are mostly seeking high net worth individuals… A Schwab brokerage account is free, and the Schwab Investor Checking is a fantastic checking account in its own right. I originally looked at Schwab as a result of the Amex partnership, but I’d continue to use them as my primary bank even without Amex.)

One of the pleasures of a new Amex card is setting up all the benefits that must be added manually. For any card that earns airline incidental fee credits, that means manually selecting an airline. I’ve always picked United in the past, since Gift Registry contributions are usually reimbursed… although with United’s Gift Registry page unavailable for the past couple months, I’m considering switching to American and trying my hand with e-gift cards.

However, any time I have tried to select American with my new card in the past few weeks, I have received this error message:

Anyone else dealing with this? The end of the year is rapidly approaching, so I’m hopeful that Amex fixes it soon. I can always try calling, but I’m lazy. That’s why I’m writing this whole blog post rather than taking the same amount of time to call Amex and resolve it.

I made the switch this year from Amex’s normal Platinum card to the newish Charles Schwab Platinum card, mostly because I wanted to get another sign-up bonus. After Amex revamped the Platinum card and raised the standard bonus from 40k to 60k, the Schwab card followed suit, so when it came time to renew my Platinum card this year, I canceled it and opened the Schwab card instead. It seemed like an even trade, since the Schwab card has all the same benefits – the only downside is that it doesn’t offer referral bonuses… although my wife was the only person who ever used my referral link, so I don’t see that as a great loss.

Otherwise, the Schwab Platinum is identical to the normal one, down to the look and feel of the card, the welcome packet, and the benefits… save for two special enhancements for Schwab customers. The first really only benefits rich people – if you have $250k/$1M with Schwab, you get $50/$200 off your annual fee. If you aren’t sitting on that kind of wealth, you pay full price like anyone else. The second benefit is “Invest with Rewards,” which enables you to convert points to cash in your Schwab investment account at rate of 1 point to 1.25 cents.

When I originally signed up for the Schwab Amex, I didn’t really think much of the points-to-cash conversion, since I generally feel like my points are worth more than 1.25 cents apiece. However, gaming out various travel scenarios and comparing the utility of this feature against other cards, it turns out that it can really work out in your favor.

For a quick recap, here’s how it works. When you add the Schwab Platinum to your Amex online account, you’ll see an “Invest with Rewards” option under the normal “Explore Rewards” button:

Clicking that will take you to a page with some general info about the program:

And once you enter some basic card info, you’ll get to select how many points you want to transfer to your Schwab account (in a fairly convoluted manner, I have to say):

That’s basically it. I didn’t end up making the transfer, but I went through all the steps before writing this post, mostly to confirm that my entire Membership Rewards balance would be eligible and that Amex wouldn’t limit it to the points I earned with this specific card.

So let’s think about this. If Amex points are worth 1.25 cents in cash, right off the bat they become a lot more useful for strategic travel redemptions. I’m thinking along the lines of using Chase Sapphire points for cheap hotel stays or short-haul flights in situations where you don’t want to pay cash. Flexibility-wise, Amex points are even better, because they’re as good as cash – you aren’t locked into a specific travel portal in order to get the 1.25/1.5-cent redemption value offered by Chase. (Chase points can be redeemed for cash too, but only at a one cent per point value.)

When the Sapphire Reserve came out, a lot of hay was made over the fact that if you combined the Freedom Unlimited and the Sapphire Reserve, you could guarantee yourself at least 2.25% cash back toward travel on every transaction (because the Freedom Unlimited earns 1.5 points per dollar, which works out to 2.25 cents toward travel when transferred to the Sapphire Reserve). However, Amex one-ups this if you add in the new Blue for Business card, which earns 2 points per dollar on all transactions up to $50k per year. That means that the Blue/Schwab combo gets you a minimum of 2.5% cash back period – not just for travel and not just through one specific portal.

2.5% back on everything is a fantastic return. The only other comparable card is the Alliant Visa Signature, which offers 3% cash back the first year and 2.5% each year thereafter. Otherwise, the closest would be the new Bank of America Premium Rewards card, which earns 1.5% or more depending on how much you bank with BofA. However, in order to get the maximum return (2.625%), you’d need to have over $100k on deposit with them. Any less, and you’re better off with Amex.

And, that’s just the return on everyday spending. Leveraging Amex’s entire card portfolio and the attendant bonus categories can really juice your overall cash-back returns.

Airfare and hotels booked through Amex: 6.25%

Groceries: up to 6% if you use a card with an annual fee; 3.75% otherwise

Gas: 3.75%

Everything else: 2.5%

(Quick aside that I’m of course ignoring the Platinum’s high annual fee here. To me, the card justifies its fee in other ways, so I’m not factoring the fee into these calculations. If you simply want cash back, you’re probably best off with a straight 2% cash back no-fee card or the Alliant Visa.)

This is important to me, because I find Amex points to be substantially easier to earn than Chase, just due to the sign-up bonuses available – and especially in the age of 5/24. If you’re maximizing your Freedom and Ink 5x categories with Chase, you’re going to do pretty well, but there are just so damn many Amex cards, I think it’s way easier to build up a six-figure balance in a short period of time. Plus, Amex is more generous with incremental bonuses (such as the 5000-point Amazon Prime renewal offer) and referral bonuses. So, given that Chase points are harder for me to earn, I’d rather save them for aspirational redemptions via unique partners like Korean Air than using them at $0.015 for dink-and-dunk flights or hotel rooms.

Amex has always offered such a vastly inferior value proposition ($0.01 for flights and $0.007 for hotels) that I’ve never considered redeeming Membership Rewards points through their travel portal. However, with this Schwab wrinkle, they become almost as valuable as Sapphire Reserve points, giving me a new option for low-value redemptions that can take some pressure off of my Chase balance. Staying within the world of travel, it’s also really important to consider that low cost carriers don’t always show up in the banks’ booking engines. If you’re looking for a flight around Europe and you want to book through Chase, you’re going to have to redeem your Sapphire Reserve points for flights on legacy carriers that are often 2-3x the cost of what you can find on Norwegian.

It’s an even bigger deal when you look at transatlantic flights. For instance, I’m brainstorming a trip with Justine next year to Venice, and I’m thinking about starting the trip in Rome. You can’t fly direct to Rome from San Francisco, but Norwegian operates direct flights from Oakland. That means that I could transfer 85,000 points to Delta in order to connect via Amsterdam or Paris, with 10 hours in a flat bed and 2 hours in Euro-business glorified economy seats… or I could pay cash to fly direct in Norwegian’s premium cabin, which isn’t as nice as business but is nicer than premium economy on Delta, Air France, or KLM.

Those Norwegian flights go for $700 – $850, so let’s imagine that I need to spend $1700 for two tickets. That means I’d have to transfer 136,000 points to cover the charges. That’s 68,000 points per person, or a substantial discount off of what you’d have to pay in Delta miles. The experiences aren’t totally equivalent, since business class on a normal airline is substantially better than Norwegian. However, considering a direct flight vs having to connect (especially given the shit-tastic quality of intra-Europe business class) does bring the two options closer in line with each other. It also means I have way more flexibility planning the trip and don’t need to worry about finding saver availability.

Consider also that if I pay for the Norwegian flights with my Platinum card, I’ll earn 8500 points, bringing the total per person down to 63,750 points. That’s roughly equivalent to what I’d have to spend if I transferred points to Flying Blue (assuming I do so before Flying Blue self-fucks their program with an iron rod), although in this scenario, I’d also avoid paying $250-$300 per person in fuel surcharges.

The Schwab Platinum card isn’t the only Amex card to offer interesting redemption options for Membership Rewards points, by the way. The Business Platinum does have the compelling benefit of offering a 35% rebate on pay-with-points travel redemptions, but there are some catches. First, of course, you’re locked into Amex’s travel portal. But even if you assume you’d be able to book those Norwegian flights, you’d then have to have 170,000 points in your account in order to purchase the flights, and you’d have to wait for the 59,500 points to be credited back to you. Ultimately you’d pay right around 55,000 points per ticket, which isn’t even that much less than the Schwab option described above.

Low-cost premium cabins like Norwegian’s and the new seats supposedly coming to WOW Air will be increasingly important to me as more and more opportunities for aspirational redemptions dry up. Just look what’s happening with Flying Blue and British Airways Executive Club… Chart-based redemptions aren’t going away immediately, but the process is definitely picking up steam. All along I have said that once chartpocalypse finally comes, I’ll turn my focus to working cash back cards in order to afford the cost difference between economy and premium on low-cost carriers. Now I’m realizing how lucrative the Schwab Amex can be in this scenario.

In the end, I’m not going to forsake transferring points to frequent flyer programs or anything – I’m just happy that I more or less stumbled into a new redemption option for my points that can make a lot of sense in certain cases.

(Finally, in case you aren’t familiar with Schwab, it’s actually really easy to get an account with them. It isn’t like Morgan Stanley or Ameriprise that are mostly seeking high net worth individuals… A Schwab brokerage account is free, and the Schwab Investor Checking is a fantastic checking account in its own right. I originally looked at Schwab as a result of the Amex partnership, but I’d continue to use them as my primary bank even without Amex.)

Support your windbag!

This site is ad-free, because I think ads are ugly. That's why I rely on readers for support! If only one person per year gives me $5, then I'll have $5 more per year. Everyone wins!

I recently stayed at the LondonHouse Chicago, which is Hilton’s Curio Collection hotel in Chicago. I liked it enough to write a real review and not some sarcastic grousing about how I hate taking pictures of hotels or how hotel reviews drive me crazy. I still hate taking pictures of hotels, though, so I apologize for the shitty pictures in this review. The takeaway is that the LondonHouse Chicago is a great hotel, and I heartily recommend it.

The setting of the hotel is pretty dramatic – right on the river, right across the street from the majestic Fuckface building, which is one of the tallest buildings in Chicago and also hands-down the fuckface-iest. But, if you turn left or right, the view is pretty good. The one annoying thing about the entrance is that the hotel’s overhang is only around three feet wide, so when it’s raining, it’s impossible to not get wet. That wouldn’t really matter if there were a lobby just inside, but there isn’t – the entrance is a narrow hallway that leads to a staircase, so there’s nowhere to stand while, say, waiting for an Uber to take you to your parents’ place.

The lobby is on the second floor and consists of a fairly small mixed-use space that includes check-in desks, a concierge desk, a bar with some really nice top-shelf liquor (at top-shelf prices, but it’s a hotel bar, so what did you expect), and a business center.

I have Hilton Honors Gold status through my Citi Reserve Hilton card (as well as my Amex Platinum), and the hotel offered me a choice between a one-category upgrade from the junior suite I booked or a discounted upgrade to a nicer suite with a river view. Since I was only staying a couple nights, I declined the upgrade altogether, since I had booked a corner junior suite, and it seemed like the best option overall. The guy checking me in told me that was the right decision, and that the base-level one-bedroom suites aren’t as nice.

Let me say a thing about the decor here before going on. When I first got into points and miles, I hadn’t really stayed at any luxury hotels before, so I didn’t have much of a preference either way of what “type” of luxury I preferred. (Go ahead and leave your FIRST WORLD PROBLEMS comment below, I’ll wait.) Now that I have a better basis for comparison, I really appreciate how the LondonHouse’s overall decor is refined while still having a lot of personality. Consider, for example, the Park Hyatt up the street, where the atmosphere is so dark and monastic that I half expected to find Paul Bettany self-flagellating off to the side as I approached the check-in desk. On the other extreme, there’s the W, which goes so far out of its way to be hip and cool and social and young and hip and cool that you wish it had nuts so you could kick it in the nuts. The LondonHouse balances these two poles really successfully, which is a big reason why I liked it so much.

The corner suite I was in is basically one big room with a partition in the middle; there’s a desk and sitting area on one side and a majorly comfy bed and ginormous TV on the other. There’s also a really long, unnecessary hallway that leads into the room. Here are a bunch of photos:

This slideshow requires JavaScript.

One nice thing about the room is that there are windows all around, although that becomes annoying when you go to close the shades and have 15 individual curtains that need to be closed. Seriously this room has more curtains than I’ve ever seen in one place.

The bathroom is pretty basic, and it definitely sets the room apart from somewhere like the Park Hyatt, where the bathroom is the same size as the rest of the room. That said, for one person on a two night stay, I didn’t need a spa tub or whatever, so it was fine. There were also little bottles of lotion, body wash, shampoo, and conditioner. Oh and a free loofah! Also, I appreciated the dental kit, since I actually forgot to bring a toothbrush.

Okay, so that’s the room… what else? Pretty good on-demand movies that I didn’t watch, and I always like a Nespresso machine instead of a Keurig. There’s a fridge but no minibar, which meant that I had to walk in the rain across the river to Walgreens to buy myself some treats (although I saved lots of money in the process, of course). Again, the bed was comfortable AF and even had the LondonHouse logo imprinted on the linens. Class all the way!

Normally I get annoyed when hotel reviews dedicate a lot of space to elite benefits like free breakfast and shit, but since Hilton Gold status is so easy to get (just open a Hilton credit card), I’ll talk about the free breakfast for elites. It was… not great. There’s a restaurant on the first floor that has a separate section of the menu for Hilton elite members. I would have preferred if they just gave you a credit toward the bill, but the vegan oatmeal was fine. The Hilton options are also on the paid part of the menu, and so I was able to figure out that the value of the free breakfast works out to around $12-15 after you account for tax and tip. One annoying thing is that the restaurant can’t charge the bill to your room, so if you want anything else, you have to pay for it there.

I think that’s it. Oh wait, there’s one more HUGELY important thing I forgot… the main feature of the hotel is its 21st floor tri-level bar, which is supposedly spectacular. Unfortunately the bar was closed due to weather during my stay, so I didn’t get to see it. However, if I enjoyed the hotel as much as I did without the bar, then it must be a pretty damn good hotel.

In this part of Chicago, I have stayed at the Swissotel, the Hyatt Regency, the Radisson Blu, the Intercontinental, and the Park Hyatt. Of all of those, this hotel was definitely my favorite… and for around 1/2 the cost of the Park Hyatt at that. Now that I’m loyal to Hilton, I’m interested to try the Conrad up the street, but it’s usually pretty expensive, whereas the LondonHouse is often a fantastic value given how expensive hotels in this area can be.

Go stay at the LondonHouse. You’ll like it, I promise.

Edit (the next morning after I posted this): Turns out it isn’t just me, but it’s also not as nefarious as I was hoping it wasn’t. Delta has acknowledged that there’s an error and they are looking into it… And while they haven’t confirmed to me directly, sources inside the company are implying that they’re very sorry for the inconvenience.

I FEEL LIKE I’M TAKING CRAZY PILLS. I’m sure I must be doing something wrong here, since it can’t possibly be true that Delta is suddenly blocking online access to partner awards. Surely this little turd of a blog wouldn’t be the first place to uncover that, right?

Let me back up. I’ve been tinkering with Delta.com a lot lately, playing with different searches and routings the same way you’d try to learn and practice a musical instrument. And every time I mess around with it, something weird happens. First it was the pricing quirk that causes saver awards to get buried in the search results under ridiculously priced standard awards. Then it was not being able to find any China Airlines awards despite there being plenty of availability on ExpertFlyer.

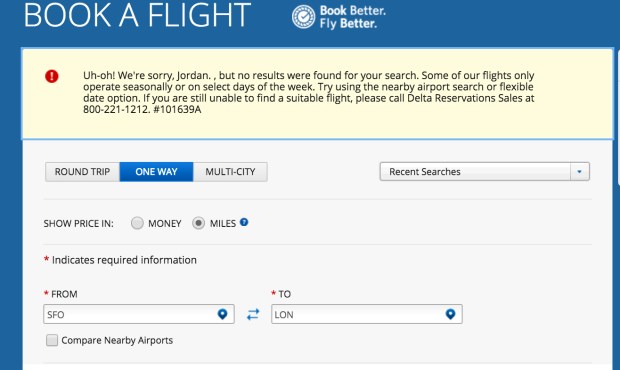

Tonight, though, I realized that I can’t get any partner awards to show up. Delta is still showing awards on their own metal, so this isn’t a general issue with their search results. Even routes that routinely show availability (like SFO-LHR on Virgin Atlantic) are coming up empty. And here’s the thing – if you search a route that Delta doesn’t fly directly, the search engine chokes. SFO-LON brings up this shitty screen (as does SFO to anywhere in Europe, since Delta doesn’t fly long haul from here):

It’s not just partner awards, though. Delta actually won’t show you any transatlantic awards with connections, regardless of whether or not it’s on Delta. For example, take SFO-SLC-CDG. Searched separately, you can find space on SFO-SLC and on SLC-CDG, but the search engine will no longer combine those two legs into a single award. It’s not an SFO issue either – repeating the ORD-AMS searches that I did last month in my post about that pricing quirk leads to the same error message. Last fall, I flew SFO-SEA-AMS, with both legs on Delta; now, searching SFO-AMS to try to find that itinerary leads to the same error message. I’ve tried different browsers and searching while logged out as well as logged in, and I can’t get the fucking thing to work.

I searched multiple cities between the US and Europe – the only ones that don’t error out are Delta hubs. In places like JFK where both Delta and Air France serve the same route, the only flights that display are Delta’s. It’s as if the search engine has the “non-stop” and “Delta only” options hard-coded into the search, regardless of how you set up the search parameters.

Here’s what’s weird, though – this is just for international flights. Searching SFO-ORD (a route that Delta doesn’t fly directly) yields the expected calendar of awards with stops. Changing ORD to any city in Europe leads to the error, though. That’s why this seems like less of a bug in the search engine and more of a deliberate attempt to shut off availability on partners or domestic connections that feed Delta long-haul routes. (I should also point out that this is only an issue with award searches. If you search for a cash ticket, you’ll find the normal array of flights, both on partners and on Delta.)

So I say again… what is going on here? Did Delta suddenly change how you search for awards and not tell anyone? Hopefully Delta’s phone agents can see the whole picture and not just Delta non-stop awards; otherwise my stash of SkyMiles just got a whole lot less useful. And here’s what really pisses me off – Delta has joint ventures with Air France and KLM and owns more than half of Virgin Atlantic (via their own 49% plus 3rd-party ownership stakes), so there’s no reason whatsoever why they should suddenly make it impossible to book awards on those carriers using SkyMiles.

As stupid as I’ll look if it turns out that I forgot to check the “Delta doesn’t suck” box on the advanced search page, I’m hoping this problem is due to my own incompetence rather than Delta’s quest to be the most customer-unfriendly loyalty program ever devised.

Amex currently has a targeted offer for 5000 points after renewing an Amazon Prime membership for $99. Originally, the offer showed an expiration date of 3/2/2018, even though there was mention in the terms of an earlier date. Here’s a screenshot of the original offer:

However, a friend told me that the March date had disappeared from her offer entirely, so I went into my account to check. Looks like the same thing happened to me – now the expiration is 1/31/2018, with no mention anywhere of the original date. I’m kind of surprised that Amex would change the terms after I added the offer to my card, although I guess they would claim they were correcting an error (since the 1/31 date was in the fine print, if not the display header).

It’s still a good offer, but if you were planning on renewing your Prime membership in February or March, definitely double check your account to make sure the expiration hasn’t moved up.

I don’t usually post about Amex offers, since other blogs usually send out the bat signal as soon as any good offers become available. However, I found this offer on one of my cards today, and a quick search didn’t show any other blogs covering it yet.

This was on a card I don’t check very often, so maybe this is old news? The expiration date is pretty soon, which suggests it may have been around for a while. In any case, check your Amex cards for this one… $20 at any small business should be pretty easy, and 1000 points is a fantastic bonus for such a small spending commitment.

“I certainly don’t want to go there just because we can fly in first class. That’s literally the worst reason to go anywhere.” So spake my precious, precious wife, who tolerates my obsession with points and miles because no one doesn’t like traveling in first class, even though she could probably take it or leave it.

I’ve been thinking about this post for a long time, but I haven’t gotten around to writing it, because I’m lazy. However, I had my worst day of viewership on the blog since late in 2016 yesterday, which tells me my ten(s) of loyal readers are hungry for new content. So here you go.

To kick things off, if you’ve never read this article on The Deal Mommy about “Vendoming,” you definitely should. Basically, she defines Vendoming as the points and miles blogger check-off circuit: Park Hyatt Vendome, Etihad Apartments to the Park Hyatt or St. Regis Maldives, Hilton Conrad Koh Samui, and of course a first class product where you get to choose between Dom Perignon and Krug. Criticizing Vendoming has less to do with a specific criticism of any of those things; it’s more an indictment of the way certain travel experiences get elevated via groupthink to become the supposed pinnacle of global travel.

I’m ambivalent about this: on the one hand, I wholeheartedly agree with this sentiment, but at the same time, I’m guilty of it. I really wanted to stay at the Park Hyatt Vendome, because I love Paris and had never stayed at a hotel anywhere near that fancy before. As I’ve said many times, the #1 reason why I bother with points and miles is to unlock travel experiences like this, since it’s very unlikely I’d ever be able to afford paying for them outright. The underlying conceit of that justification, however, is that luxury travel matters to me in the first place. On the other hand, to many people, a Motel-6 equivalent is fine as long as they get to see a new place.

While the teenage punk rocker in me sometimes cringes at what a yuppie wannabe I’ve become, I don’t think any one style of travel is right or wrong. Personally, I enjoy travel more when I can do it in luxury, but that certainly doesn’t stop me from traveling to places where the luxury travel industry doesn’t exist (like the Faroe Islands). But if someone else doesn’t ever want to be out of range of a 5-star resort, what’s really so wrong with that? I mentioned this in a past post about WOW Air, but there’s definitely a budget travel corollary to the luxury-only yuppie: the masochistic “we took 17 connections and overnighted in five airports in order to go to Ghana and back for $175” person who wants everyone to know how hardcore they are.

The issue here is speaking truth to power about the Vendoming circuit, since (speaking from experience), it’s definitely true that the points & miles blogging community does seem to prize the same products and experiences above all others. And even if these experiences are among the best in the world, too much time spent in the blogosphere can cloud your judgment, the same way reading Boarding Area blogs every day for a year will make you want a Rimowa suitcase.

With all that in mind, I want to come back to my wife’s contention that being able to fly somewhere in first class is literally the worst reason to go anywhere, since it definitely ties back into the issue of Vendoming. For instance: if you have no desire ever to go to Abu Dhabi, it would probably be dumb to spend a large chunk of your hard-earned miles on flights in first class on Etihad’s A380 just because many consider it the world’s best first class product.

However, for me the line between wanting to go somewhere and not wanting to go somewhere isn’t that cut-and-dried. In fact, while there are a number of places I really want to go, there are many more places I really haven’t put all that much thought into one way or another. Here’s an example: despite hearing good things now and then, I’ve never really thought about whether I’d ever want to visit Korea. In the course of my blog-reading, Korean Air (and Asiana) first class comes up a lot, and while they aren’t generally considered among the absolute top tier of first class experiences, they’re pretty close. I also happen to have a bunch of Korean Air miles with no immediate plans to use them, and Korean Air first class availability is fantastic.

In other words, I could put together a week in Seoul with very little effort – 80k for Korean Air one way, some hotel points for one of the many Hilton/Hyatt/IHG options, and 90-120k for Asiana back to the US (depending on whether I booked with ANA, Aeroplan, or United). Because availability is wide open on both carriers, I wouldn’t have to dick around with ExpertFlyer alerts and whatnot; I could just pick a week and book the entire thing in 15 minutes.

Okay, so let’s say I do that — I pick Seoul as a destination simply because it’s easy to fly there in first class, and I have the miles for it. What’s so wrong with that? Ever since that switch in my brain that causes me to be obsessed with something was flipped, I’ve been doing all this research about Korea, and it sounds amazing. I’ve never been to Asia; in fact I’ve never been anywhere where the alphabet wasn’t the same one I’m used to. At this point, I really, legitimately want to go to Korea, so is it something I should be ashamed of that the impetus for this desire happened to be how easy it was to fly there in first class? Pushing this line of thinking further, the whole luxury travel thing could even be seen as a net positive when it comes to me seeing the world, since my aversion to long-haul flights in economy would normally cross most of the other side of the Pacific off my list just because the idea of flying there and back would stress me out too much.

I’m not sure how much my newfound desire to go to Seoul dovetails with Vendoming, since it’s not like blogs breathlessly talk about how great Korea is… although one of the ads I saw ALL THE TIME on Facebook when the Chase Sapphire Reserve came out was a picture of The Points Guy sitting in Korean Air first class, touting it as a great way to spend the six-figure sign-up bonus. So while it may not be a level-1 Vendoming destination, it’s still definitely in the constellation of experiences exalted by the points and miles blogosphere.

I’ll give another example, this one involving Emirates first class. Everyone knows Emirates first class, thanks to their huge ad campaign, and it sometimes feels like you can’t call yourself a legitimate points and miles enthusiast until you fly Emirates first. Given the relative cost and difficulty of booking Emirates first after Alaska’s no-notice devaluation, I figured I probably would never get around to it (well, that and I didn’t have any immediate need to go to Dubai).

I forgot about Emirates’ fifth freedom flights, though, including their flight from Milan to JFK that can be booked for 85,000 Emirates Skywards miles (Amex transfer partner) and around $300 in fuel surcharges. Given the way the devaluation winds have been blowing lately, that’s around what you’d pay to book Air France’s shitty angle-flat business class through Delta. United would charge 70,000 for Lufthansa business (57,500 for their own flights, but let’s be realistic – United doesn’t release space on their own flights). It’s not like it’s a screaming deal or anything, but it’s still within the realm of what I’d call reasonable.

So, here’s the opportunity to check Emirates first class off my list – I just need a reason to go to Italy. Justine and I both have a list of dream destinations, and when we go on trips, we look for places we’re both dying to visit. One of Justine’s top trips is to go to Venice, although for one reason or another, it was never at the top of my list. Nothing against Venice, there are just too many other places I want to go.

In this case, the Emirates angle gave me the push I needed to go ahead and plan a trip to Venice over Justine’s birthday next year. She doesn’t know I’m planning the trip (don’t worry, she doesn’t read this blog), so I’m going to try to keep it a surprise as long as I can. It should be a really great trip, capped off with what hundreds of blogs have promised me will be the most amazing flight home. Dream trip for her, fun plane for me (and I’m sure I won’t mind Venice either).

Anyway, I guess my point at the end of all this is to make sure you’re not traveling just to fulfill some frequent flyer checklist… but I also don’t think it’s insane to let aspirational travel experiences influence your trip planning. Maybe it starts with you picking a particular flight or airline, but hopefully it ends with you getting to visit a great destination that you hadn’t really thought much about before.

In the past, I have had no trouble finding China Airlines partner awards on Delta’s site, and availability is often wide open. Unfortunately, it looks like Delta’s search engine is having trouble seeing that award space these days, for whatever reason. Hopefully this is a situation where you can call in to have a customer service rep book the flight for you; otherwise SkyMiles just got a little bit less useful.

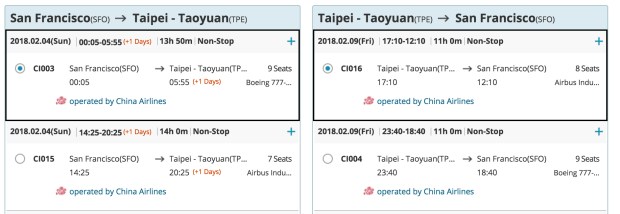

Here’s China Airlines availability in early February 2018 on ExpertFlyer:

And although I only searched ExpertFlyer for one person, an award itinerary for that date range through Korean Air’s site shows a veritable cornucopia of award seats:

However, searching Delta generates one of these two error messages, both of which seem to express shock and surprise that Delta’s search engine is a piece of shit. Uh oh! Oh no!

I’ve tried various cities, different dates, flexible date searches, individual date searches, different cabins, etc and nothing comes up. Maybe I’m doing something wrong and need to go reread the hundreds of tutorials online that cover booking SkyTeam awards on Delta, or maybe the problem is on Delta’s end.

Clearly China Airlines isn’t blocking award availability to partners, since you can book via Korean. Maybe it would be easier just to do that, but the prices are similar – 80k on Delta the last time I checked (although it might be more now I WOULDN’T KNOW SINCE I CAN’T GET ANY FLIGHTS TO COME UP ONLINE) vs 77,500 on Korean. Problem is, Korean miles are much more valuable and I personally would save them for first class SkyTeam awards, which Delta won’t let you book at all. Plus, Korean won’t let you book one way partner awards, so you’d need to cough up 155,000 miles for the round trip.

Has anyone else run into this? Are there workarounds I’m not trying? The one thing I am trying is not to hate Delta, but they make it hard sometimes.

{kind=link}